Contents:

Executive Summary

Overview and Trends

Market Overview

Market Structure

Insurance Premiums

Key Events in the Indian Insurance Market

Review of Major Market Players

Life Insurance ($95 billion)

- Life Insurance Corporation of India (Revenue: $58 billion)

- SBI Life Insurance Company ($8 billion)

- HDFC Life Insurance Company ($7 billion)

- ICICI Prudential Life Insurance Co. ($5 billion)

- Max Life Insurance Company ($3 billion)

- TATA AIA Life Insurance Co. ($2.5 billion)

- Bajaj Allianz Life Insurance Co.

General (Non-Life) Insurance ($31 billion)

Public Sector Companies ($10 billion)

Private Sector Companies ($16 billion)

Health Insurance ($3.2 billion)

Specialized Insurance ($1.9 billion)

—————————-

Executive Summary

- The Indian insurance market is open to foreign investment (with minor restrictions), resulting in significant presence of international insurance groups (e.g., Allianz, AIA, MetLife).

- Life insurance accounts for 75% of the sector’s total revenue. Of this, the state-owned Life Insurance Corporation (LIC) alone generates 61%.

- In the general (non-life) insurance segment, private companies affiliated with major Indian conglomerates (SBI, HDFC, ICICI, TATA) dominate the market.

- Equity ownership in most insurance companies is widely dispersed among investment funds, with no clear controlling shareholders in many cases.

- Among individual beneficial owners, the prominent business families include Tata, Bajaj, Birla, and Pai.

Overview and Trends

Market Overview

India ranks as the 10th largest life insurance market globally and the 4th largest general insurance market in Asia (14th worldwide).

Over the past 20 years, the Indian insurance sector has experienced impressive growth, driven by increased private-sector participation, improved distribution channels, and significant gains in operational efficiency.

In the last nine years alone, the sector has attracted nearly ₹540,000 crore (US$6.5 billion) in foreign direct investment (FDI), thanks to the government’s gradual liberalization of foreign capital rules.

- In 2013, the Insurance Regulatory and Development Authority of India (IRDAI) raised the FDI cap in insurance from 26% to 49%.

- In 2021, the cap was further increased to 74%.

- Insurance intermediaries are permitted 100% foreign ownership.

Key growth drivers include economic expansion, a rising middle class, technological innovation, and supportive regulation. According to Swiss Re, one of the world’s largest reinsurers, India’s total insurance premiums are projected to grow at a real annual rate of 7.1% from 2024–2028—significantly outpacing global (2.4%), emerging market (5.1%), and developed market (1.7%) averages. This positions India to have the fastest-growing insurance sector among G20 nations.

Per S&P Global Market Intelligence, India is the second-largest Insurtech market in the Asia-Pacific region, accounting for 35% of all venture capital investments in the Insurtech sector.

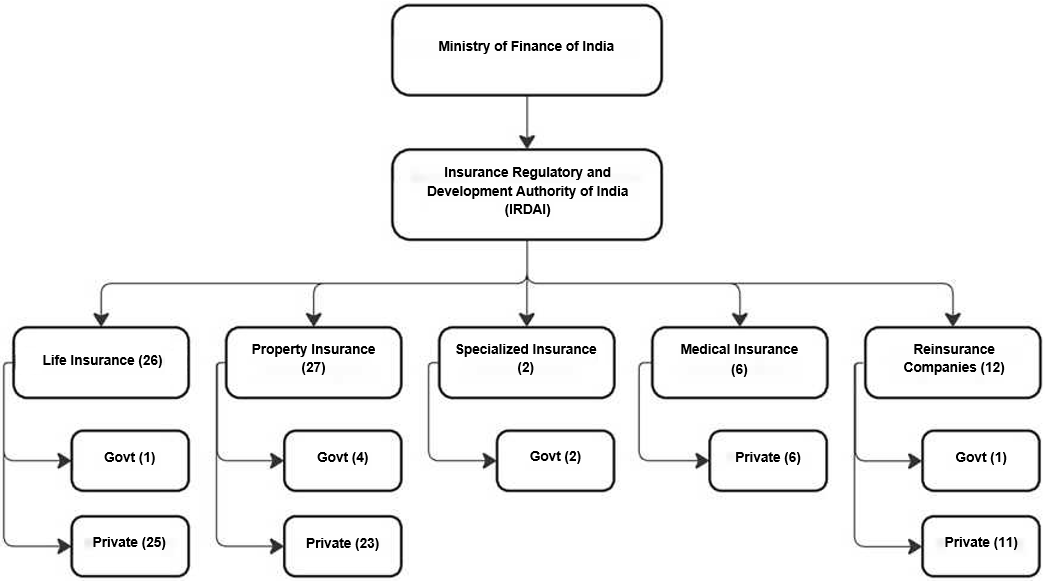

Market Structure

As of May 2024, India’s insurance industry comprised 57 insurers:

- 24 life insurers

- 34 non-life (general) insurers

In the life segment, Life Insurance Corporation (LIC) is the sole public-sector player. Established in 1956 through the nationalization and merger of 154 Indian and 16 foreign insurers plus 75 provident societies, LIC held a monopoly until the late 1990s, when the sector was reopened to private players.

In the non-life segment, there are 6 public-sector insurers, in addition to General Insurance Corporation of India (GIC Re), the country’s sole national reinsurer.

Including reinsurance companies, there are 65 private insurance entities operating in India.

Other key stakeholders include individual and corporate agents, brokers, and third-party administrators (TPAs) handling health insurance claims.

The sector is regulated by the Insurance Regulatory and Development Authority of India (IRDAI), whose mandate is “to protect the interests of policyholders, to regulate, promote, and ensure orderly growth of the insurance industry and matters connected therewith or incidental thereto.” IRDAI is a 10-member body appointed by the Government of India, comprising a Chairperson, five full-time members, and four part-time members.

Primary legislation includes the Insurance Act of 1938 and the IRDA Act of 1999.

The entire insurance sector falls under the purview of the Ministry of Finance, Government of India.

Structure of the Indian Insurance Market (including foreign companies and branches, IBEF May 2024)

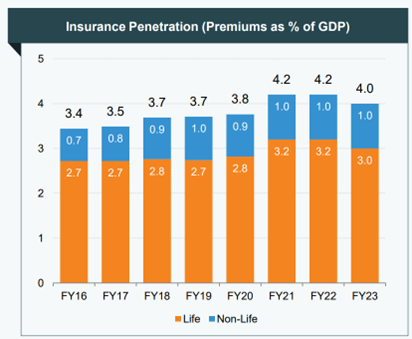

Insurance Premiums

In FY 2023, India’s total insurance premiums amounted to 4% of GDP:

- 3% from life insurance

- 1% from non-life insurance

In the life insurance segment, LIC held a 58.87% market share of first-year premiums, while the private sector accounted for 41.13%.

Among private players, SBI Life, HDFC Life, and ICICI Prudential Life lead in premium collection:

- SBI Life: ₹38,238 crore (US$4.60 billion)

- HDFC Life: ₹29,988 crore (US$3.60 billion)

- ICICI Prudential Life: ₹18,081 crore (US$2.17 billion)

Key Events in the Indian Insurance Market (2021–2024)

- April 2024: The Competition Commission of India (CCI) approved Axis Bank’s subscription to 142,579,161 shares of Max Life Insurance Company Limited.

- January 2024: CCI approved the merger of Shriram LI Holdings Private Limited (SLIH) with Shriram Life Insurance Company Limited (SLIC).

- November 2023: Zurich Insurance Group announced plans to acquire a controlling stake in Kotak General Insurance—the first major foreign investment in India’s insurance sector in eight years. CCI later approved Zurich’s acquisition of a 70% stake via Kotak Mahindra Company.

- September 2023: The UK and India agreed to establish a partnership to promote cross-market investments in insurance and pensions.

- 2022: LIC’s IPO became India’s largest-ever initial public offering and the 6th largest globally that year. By November 2022, it had raised over one-third of all capital mobilized on India’s primary equity market year-to-date.

- December 2021: Probus Insurance secured US$6.7 million in funding from a Swiss impact investment fund.

- November 2021: Willis Towers Watson (UK) acquired the remaining 51% of WTW India, taking its ownership to 100%.

Review of Major Market Players

According to Atlas Magazine (April 2024):

- Total revenue of Indian insurers in 2023: US$126 billion (4.8% YoY growth)

- In rupee terms: ₹10.4 trillion (14% YoY growth)

- Life insurance accounts for 75% of total sector revenue, with LIC generating 61% of life insurance revenue.

- In non-life insurance, private companies account for 60% of revenue.

Life Insurance ($95 billion)

The following 7 companies account for 90% of life insurance revenue in India:

- Life Insurance Corporation of India (LIC) – Revenue: $58 billion

- Founded in 1956 through nationalization of the insurance industry.

- Operates 11,300 branches and employs 2.28 million agents.

- 96.5% owned by the Government of India.

- SBI Life Insurance Company – Revenue: $8 billion

- Joint venture between State Bank of India (SBI) and BNP Paribas Cardif.

- Ownership: SBI (55.5%), BNP Paribas Cardif (0.22%), Value Line & MacRitchie (1.95% each), public float (12%).

- HDFC Life Insurance Company – Revenue: $7 billion

- JV between HDFC Ltd and Abrdn (global asset manager).

- Majority shareholder: HDFC Bank (50.37%).

- ICICI Prudential Life Insurance Co. – Revenue: $5 billion

- JV between ICICI Bank and Prudential plc (UK).

- First Indian insurer listed on domestic stock exchanges (2016).

- Ownership: ICICI Bank (51.15%), Prudential plc (22.02%).

- Max Life Insurance Company – Revenue: $3 billion

- Part of Max Group, a diversified Indian conglomerate.

- Ownership: Max Financial Services (80.98%), Axis Bank (16.22%).

- TATA AIA Life Insurance Co. – Revenue: $2.5 billion

- JV between Tata Sons (51%) and AIA Group (49%).

- Tata Group: 100+ companies, $403 billion revenue (Aug 2024); controlled via charitable trusts.

- AIA Group: Hong Kong-based, serves 33 million individual and 16 million group customers across Asia-Pacific.

- Bajaj Allianz Life Insurance Co.

- JV between Bajaj Group (74%) and Allianz SE, Germany (26%).

- Bajaj family: Among India’s top 10 wealthiest; interests in autos, appliances, steel, finance, and tourism.

- Allianz SE: Europe’s largest financial services company; global leader in risk, savings insurance, and asset management.

General (Non-Life) Insurance ($31 billion)

Public Sector Companies ($10 billion)

Four state-owned insurers—formerly subsidiaries of GIC—now operate independently after GIC’s conversion to a reinsurer under the IRDA Act (1999). They collectively hold 32.3% of the non-life market:

| Company | 2023 Revenue ($M) | Market Share |

| New India Assurance | 4,197 | 13.4% |

| United India Insurance | 2,147 | 6.9% |

| Oriental Insurance | 1,900 | 6.1% |

| National Insurance | 1,844 | 5.9% |

| Total | 10,088 | 32.3% |

Private Sector Companies ($16 billion)

Top 5 private non-life insurers—affiliated with life insurance leaders—account for 30% of non-life revenue. Combined with public insurers, they represent 60% of the entire general insurance market:

| Top 5 Private Companies | 2023 Revenue ($M) | Market Share |

| ICICI Lombard General Insurance | 2,559 | 8.2% |

| HDFC ERGO General Insurance | 2,025 | 6.5% |

| Bajaj Allianz General Insurance | 1,866 | 6.0% |

| Tata AIG General Insurance | 1,604 | 5.1% |

| SBI General Insurance | 1,318 | 4.2% |

| Total | 9,372 | 30.0% |

Health Insurance ($3.2 billion)

Health insurance is treated as a distinct segment (separate from life insurance), representing 10% of non-life revenue and 2.5% of the total insurance market.

Key players:

- Star Health & Allied Insurance – $1.6 billion (50% of health segment)

- Owned by Safecorp Investments (40%) and investor Rakesh Jhunjhunwala (14%); rest held by public investors.

- Care Health Insurance – $626 million

- Ownership highly fragmented across multi-layered investment funds; 5.3% held by Government of India.

- Niva Bupa Health Insurance – $496 million

- Dispersed ownership; no identifiable ultimate beneficial owners.

- Aditya Birla Health Insurance – $331 million

- 46% owned by Kumar Mangalam Birla, chairman of Aditya Birla Group (one of India’s largest conglomerates). Remaining shares held by investment funds.

- ManipalCigna Health Insurance – $165 million

- 51% owned by the Pai family (founded Manipal education and hospital network). Remaining stake held by small funds.

Specialized Insurance ($1.9 billion)

Only two companies operate in this niche:

- Agriculture Insurance Company of India (AIC) – 92% of segment revenue

- Subsidiary of GIC (public sector).

- India’s leading crop insurer and world’s largest by number of farmers insured.

- Holds >50% market share in India’s crop insurance segment.

- ECGC Limited

- Wholly owned by the Government of India.

- Functions as India’s export credit insurance agency, providing coverage to exporters and banks against non-payment risks.