1. Current Shipbuilding Capacity and Market Dominance

-

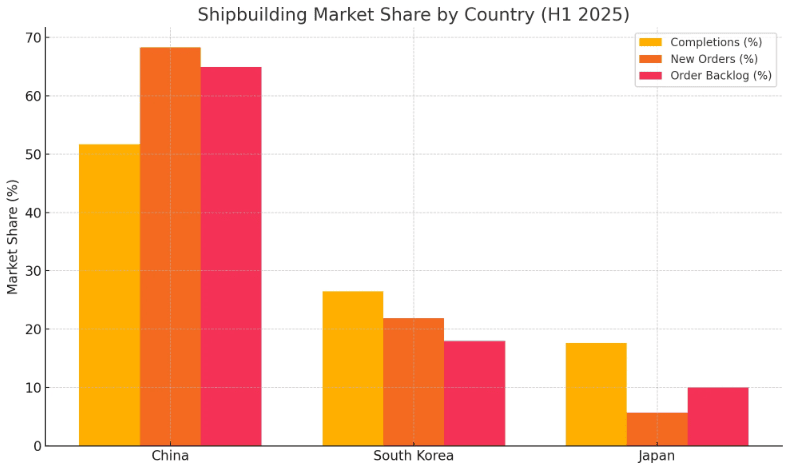

Global Leadership: China is the world’s largest shipbuilder, accounting for 51.7% of global ship completions by deadweight tonnage (DWT) in H1 2025. It also holds 68.3% of new orders and 64.9% of the order backlog.

-

2021-2025 statistics:

-

-

In 2021, China posted a shipbuilding output of 39.7m dwt, an increase of 3% year-on-year

-

In 2022, the country’s shipbuilding output hit 37.86 million deadweight tonnes (dwt) last year, accounting for 47.3 percent of the world’s total volume

-

In 2023, the country’s shipbuilding output climbed 11.8 percent year on year to 42.32 million deadweight tonnes (dwt), accounting for 50.2 percent of the world’s total figure

-

In 2024, China’s shipbuilding completion volume was 48.18 million DWT, up 13.8% year on year

-

January – June 2025: Completions reached 24.13 million deadweight tons (DWT) (↓ 3.5% YoY); New Orders totaled 44.33 million DWT (↓ 18.2% YoY); Order Backlog surged to 234.54 million DWT (↑ 36.7% YoY)

-

-

Mega-Merger Impact: The merger of China State Shipbuilding Corporation (CSSC) and China Shipbuilding Industry Corporation (CSIC) has created a behemoth with $56 billion in assets and $18 billion in annual revenue. This consolidation reduces internal competition and enhances efficiency.

-

Export Focus: 89.6% of China’s ship completions are for international clients, generating $24.5 billion in export revenue in H1 2025. Key exports include LNG carriers, container ships, and advanced naval vessels.

2. Ship Repair Capabilities

-

Global Repair Hub: China dominates the global ship repair industry, with the top 10 ship repair yards worldwide all located in China.

From January to November 2021, the ship repair industry in China earned profits of around 1.3 billion yuan

In 2021, the industry revenuewas $5.25 billion

In 2022, the industry revenueincreased by 4.5% to $5.5 billion

In 2023, the industry revenue grew by 4.0% to $5.7 billion

In 2024, the total ship repair output reached RMB 40 billion ($5.6 billion)

-

Regional Concentration: The Yangtze River Delta accounts for over 60% of China’s ship repair output, with Zhoushan City alone contributing 42.5% of the national output value.

-

Green Ship Repair: 51.7% of ship repair activities in China now incorporate green practices, including eco-friendly docking and waste management systems.

3. Technological Advancements and Innovation

-

Green Shipbuilding: China is investing heavily in eco-friendly vessels, including LNG-powered ships, ammonia-fueled carriers, and hydrogen propulsion systems. This aligns with global decarbonization goals and IMO regulations.

-

Smart Shipyards: Adoption of AI, IoT, and 3D modeling has streamlined production processes. CSSC is developing intelligent ships with autonomous navigation and predictive maintenance capabilities.

-

Dual-Use Strategy: China’s “military-civil fusion” policy allows shipyards to seamlessly transition between commercial and naval projects. This dual-use capability enhances resource allocation and technological spillover.

4. Challenges and External Pressures

-

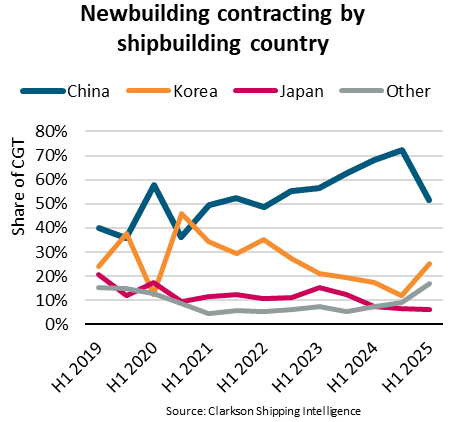

U.S. Tariffs and Port Fees: The U.S. Trade Representative (USTR) has proposed port fees of up to $1.5 million on Chinese-built ships, causing China’s market share to drop from 72% to 52% in H1 2025.

-

Competition: China’s dominant position in shipbuilding is unlikely to significantly change soon, but the country could face increasing competition in the medium term. Countries like the Philippines and Vietnam, already small-scale producers of bulkers and tankers, may boost their output, benefiting from low labour costs.

-

Geopolitical Risks: Overreliance on Chinese shipbuilding has prompted countries to boost domestic production (link 1, link 2). This could reduce long-term demand for Chinese ships.

5. Future Prospects and Strategic Goals

-

15th Five-Year Plan (2025–2030): China aims to lead in green and smart shipbuilding, with focus areas including offshore engineering, low-emission vessels, and digital integration.

-

Northern Sea Route (NSR) Development: China studies the opportunity to use NSR with Russia. For China, which depends heavily on maritime trade, shorter and cheaper routes are enormously attractive. For Russia, controlling the Northern Sea Route offers both economic benefits and strategic leverage.

-

Global Expansion: Chinese firms are acquiring foreign shipyards and forming partnerships to bypass tariffs. For example:

-

China COSCO Shipping’s majority stake in the Port of Piraeus (Greece)

-

Chinese shipyards are collaborating with Vietnamese partners to assemble ships using Chinese-made components. This helps avoid direct tariffs on “Chinese-built” vessels, as final assembly occurs in Vietnam.

Featured image by Maksym Kaharlytskyi on Unsplash