Oil production data: Worldometer (2005-2016), EIA (2017); Reuters (2018; 2020; 2024); Columbia School of International and Public Affairs (2019); TAdviser (2021); CEIC Data (2022-23); Bloomberg (2025)

Oil consumption data: Worldometer (2005-2016); EIA (2017); CIEP (2018); Oxford Energy (2019); YCharts (2020-21); CEIC Data (2022-23); Visual Capitalist (2024); World Population Review (2024)

Oil export data: CEIC Data (2012-23); Visual Capitalist (2024);

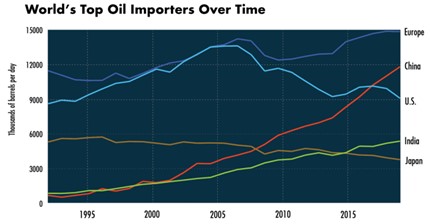

Oil import data: Index Mundi (2005-11); CEIC Data (2012-23); Visual Capitalist (2024); Oil Price (2025)

Oil Production and Consumption in China:

| Year | Produced, kb/d | Consumed, kb/d | Exported, kb/d | Imported, kb/d |

| 2005 | 3,871 | 6,970 | ~0 | 2,599 |

| 2006 | 3,980 | 7,493 | ~0 | 2,905 |

| 2007 | 4,079 | 7,923 | ~0 | 3,264 |

| 2008 | 4,167 | 8,041 | ~0 | 3,578 |

| 2009 | 4,218 | 8,497 | ~0 | 4,082 |

| 2010 | 4,575 | 9,339 | ~0 | 4,754 |

| 2011 | 4,660 | 10,053 | ~0 | 5,052 |

| 2012 | 4,773 | 10,550 | 49 | 5,424 |

| 2013 | 4,912 | 11,084 | 32 | 5,658 |

| 2014 | 5,045 | 11,637 | 12 | 6,178 |

| 2015 | 5,180 | 12,385 | 57 | 6,731 |

| 2016 | 4,905 | 12,792 | 59 | 7,625 |

| 2017 | 4,800 | 13,200 | 97 | 8,426 |

| 2018 | 3,780 | 14,000 | 52 | 9,260 |

| 2019 | 3,836 | 14,100 | 16 | 10,180 |

| 2020 | 3,870 | 14,400 | 33 | 10,853 |

| 2021 | 3,994 | 14,890 | 53 | 10,301 |

| 2022 | 4,094 | 14,970 | 41 | 10,187 |

| 2023 | 4,181 | 16,577 | 28 | 11,309 |

| 2024 | 4,240 | 16,400 | 18 | 11,100 |

| 2025 (forecast) | 4,600 | 16,500 | ~0 | 11,650 |

Analysis of crude oil production:

Crude oil production in China experienced fluctuations from 2005 to 2025, with a peak around 2015 followed by a decline and a modest recovery towards the mid-2020s.

Crude Oil Production in China averaged 3111.14 BBL/D/1K from 1973 until 2025, reaching an all time high of 4500.00 BBL/D/1K in March of 2025 and a record low of 1012.00 BBL/D/1K in February of 1973. source: U.S. Energy Information Administration

Analysis of crude oil consumption:

China’s oil demand growth in 2025 is expected to be nearly the same as last year—at just over 100,000 barrels per day (bpd), according to an Energy Intelligence analysis based on data from China’s National Bureau of Statistics and Customs.

China’s oil use will reach a maximum 16.9 million barrels a day by 2027.

China’s oil use is expected to grow by 3–4 mb/d reaching 17-18 mb/d in 2040. While China’s oil use has a strong growth potential—given that China’s per capita oil use is currently around one-third of OECD levels—future growth rates will be tempered by efforts to tackle air pollution.

Domestic production of petroleum products:

China’s oil refinery capacity grew substantially, from lower levels in the 2000s to 18.5 million barrels per day (bbl/d) by 2024. This expansion supported increased production of petroleum products.

Refinery throughput in 2024 reached 708.43 million tons (approximately 14.2 million bbl/d), reflecting a 1.6% increase from 2023. This indicates sustained demand for processing crude oil into products.

There are plans to further increase refining capacity and invest in advanced technologies (e.g., deepwater drilling and shale extraction) are expected to support production growth through 2025.

Export of petroleum products:

2005–2018: China’s exports of refined petroleum products grew substantially. In 2017, exports were valued at $25.4 billion, rising to $36.0 billion in 2018—a record high at the time. This growth was driven by expanding refining capacity and increasing global demand for diesel, gasoline, and aviation fuel.

2019–2024: Exports faced volatility due to fluctuating global oil prices, geopolitical tensions, and domestic policy adjustments. For example, in early 2025, export quotas for clean oil products (gasoline, diesel, jet fuel) were reduced by 4% year-on-year, reflecting a strategic pivot toward prioritizing domestic supply.

2025: Exports showed resilience despite challenges. In July 2025, refined oil product exports reached 5.34 million tons, a 7.1% year-on-year increase and the highest monthly volume since June 2024. Diesel exports surged 53.2% to 820,000 tons, while gasoline exports rose 18.6% to 930,000 tons.

Energy Security: By 2025, China prioritized domestic supply stability, leading to tighter export quotas for clean products but relaxed quotas for low sulphur fuel oil (LSFO) to capture marine fuel demand.

China’s petroleum product exports are expected to remain volatile, influenced by global oil prices, domestic policies, and demand from emerging markets. The shift toward high-value exports (e.g., jet fuel) and strategic quota allocations will likely continue, supporting long-term growth in specific segment.

Import of petroleum products:

2005–2015: China’s imports of petroleum products grew steadily alongside its economic expansion and rising domestic energy demand. While specific figures for earlier years are not detailed in the search results, this period saw increasing reliance on imports to fuel industrial growth and transportation needs.

2016–2024: Imports fluctuated due to global oil price volatility, domestic refining capacity changes, and policy adjustments. For example, in 2024, China imported 22.9 million metric tons of crude oil in the first five months, with a year-on-year decline of 0.7% in volume and 14.5% in value.

2025: Imports showed mixed trends. In the first seven months of 2025, crude oil imports averaged 11.29 million barrels per day (b/d), a 3.2% increase from the same period in 2024. However, refined petroleum product imports (e.g., naphtha) saw significant changes due to policy shifts and demand dynamics.

The shift toward high-value petrochemical feedstocks (e.g., naphtha) and strategic stockpiling will likely continue, supporting import volumes even as domestic refining capacity expands.

Analysis of petroleum product consumption:

2005–2015: Consumption grew rapidly, doubling from 90 million metric tons (Mt) in 1985 to 209 Mt in 2004, with an average annual growth rate of 6.7%. By 2015, consumption reached 11.5 million barrels per day (mb/d).

2015–2024: Growth continued but at a moderated pace due to economic slowdown and efficiency measures. Consumption reached 14.5 mb/d in 2019 and further increased to *** million Mt in 2024 (exact figure redacted in sources but noted as “significant growth”).

2025: Projected to maintain steady growth, with demand driven by industrial and transportation sectors. China’s consumption accounted for two-thirds of global incremental oil consumption in 2019

Consumption is expected to grow steadily but at a slower pace, influenced by:

- Economic Transition: Shift toward services and high-tech industries may reduce energy intensity.

- Alternative Fuels: Expansion of electric vehicles and renewables could cap oil demand growth.

- Global Policies: Geopolitical factors and international climate commitments will shape long-term demand

Domestic LNG production:

Trend Overview: 2005–2025

- Early Stage & Pilot Projects (2005–2010)

- Domestic LNG was virtually nonexistent before 2006.

- First small-scale LNG plants launched around 2006–2008, mainly in remote gas-producing regions (Shaanxi, Inner Mongolia, Xinjiang) to monetize “stranded gas.”

- 2010 production: ~0.5–1 million tonnes (Mt)

- Rapid Expansion Phase (2011–2017)

- Driven by:

- Need to transport gas from remote fields without pipelines.

- Government push for cleaner fuels in transport (LNG trucks, buses).

- Coal-to-gas and coalbed methane (CBM) projects feeding small LNG plants.

- Annual growth: ~30–50%

- 2017 production: ~6–7 Mt

- Maturation & Slowdown (2018–2022)

- Pipeline infrastructure (e.g., West-East Gas Pipelines) reduced need for LNG as transport medium.

- Environmental crackdowns on coal-to-gas projects slowed feedstock supply.

- Focus shifted to imported LNG to meet soaring demand.

- Growth slowed to ~5–10% annually.

- 2022 production: ~9–10 Mt

- Stabilization & Niche Role (2023–2025)

- Domestic LNG now serves niche markets: heavy trucking, remote industrial users, peak-shaving, and backup supply.

- No major capacity additions; focus on efficiency and integration with renewables/hydrogen.

- 2023 production: ~10.5 Mt

- 2024 (est.): ~11 Mt

- 2025 (proj.): ~11.5–12 Mt — plateau expected as pipeline grid expands and EVs replace LNG trucks.

LNG export:

No credible plans to export LNG before 2030.

Even if China develops massive shale gas or offshore resources (e.g., South China Sea), domestic demand will absorb all volumes.

LNG import:

Trend Overview: 2005–2025

- Pioneering Phase (2006–2010)

- First LNG import terminal: Guangdong Dapeng (joint venture with BP/CNOOC), started in 2006.

- Imports began at small scale — mainly to supply Pearl River Delta.

- 2010 imports: ~9 million tonnes (Mt)

- Rapid Expansion (2011–2017)

- Driven by:

- “Coal-to-gas” policy to reduce urban air pollution.

- Industrial and residential gasification.

- Limited domestic pipeline gas supply.

- New terminals built along east/south coasts: Fujian, Shanghai, Jiangsu, Zhejiang.

- Annual growth: 20–30%

- 2017 imports: ~38 Mt — China becomes world’s #2 LNG importer (after Japan)

- Boom & Diversification (2018–2021)

- Import growth accelerates as Beijing pushes “Blue Sky” campaign.

- U.S.-China trade tensions briefly disrupted U.S. LNG flows (2019), but rebounded post-2020.

- Long-term contracts signed with Qatar, Australia, Russia (Yamal), U.S.

- 2021 imports: ~79 Mt — China surpasses Japan as world’s #1 LNG importer

- Volatility & Adjustment (2022–2023)

- 2022: Imports fell to ~63 Mt (–20% YoY) due to:

- High global prices post-Ukraine war.

- Economic slowdown + strict zero-COVID policy.

- Industrial demand destruction.

- 2023: Partial recovery to ~71 Mt (+13% YoY) — price normalization, post-COVID rebound, stock rebuilding.

- Stabilization & Strategic Growth (2024–2025)

- 2024 (est.): ~76–78 Mt (+7–10%)

- 2025 (proj.): ~80–85 Mt — continuing infrastructure expansion and gas-for-coal switching.

- Focus shifting to:

- Contract diversification (reduce reliance on Australia/Qatar).

- Floating storage and regasification units (FSRUs).

- Strategic reserves and flexible offtake.

Domestic LNG consumption:

Trend Overview: 2005–2025

- Birth of LNG Market (2006–2010)

- LNG consumption began in 2006 with the launch of Guangdong Dapeng terminal.

- Early use: city gas in Guangdong, Fujian; no industrial or transport scale yet.

- 2010 consumption: ~10 Mt (mostly imported)

- Acceleration Phase (2011–2017)

- “Coal-to-gas” policy drives massive gas switching in heating and industry.

- LNG truck market booms — thousands of LNG refueling stations built.

- Coastal provinces (Jiangsu, Zhejiang, Shandong) build terminals.

- 27 million metric tons consumed in 2015

- 2017 consumption: ~45 Mt

- Peak Growth & Diversification (2018–2021)

- Winter gas shortages → national push for LNG as flexible supply.

- LNG bunkering (marine fuel) begins in Yangtze River and ports.

- Industrial parks adopt LNG for ceramics, glass, metal processing.

- 84.7 million metric tons consumed in 2019

- 2021 consumption: ~85 Mt — surpasses Japan as world’s largest LNG-consuming nation.

- Correction & Recovery (2022–2023)

- 2022: Consumption drops to ~73 Mt due to:

- Record high global LNG prices → demand destruction in industry.

- Zero-COVID lockdowns → reduced transport and factory activity.

- 2023: Rebounds to ~82 Mt — price normalization, inventory rebuilding, policy support.

- Maturing Market (2024–2025)

- Consumption growth slows but remains positive.

- Focus shifts to:

- Peak-shaving and storage (LNG as grid balancing tool).

- Heavy transport (though challenged by EVs).

- Replacing diesel in remote/off-grid industrial applications.

- 2024 (est.): ~88 Mt

- 2025 (proj.): ~92–95 Mt — approaching plateau before energy transition accelerates post-2030.